What’s Driving Mortgage Rates Today?

Mortgage rates today have edged up. (Many lenders raised rates late yesterday after the Fed meeting adjournment. Those that did not increase pricing yesterday will probably raise rates this morning.)

Today’s reporting didn’t do much to improve the situation. First, the Labor Department reported that US worker productivity fell by .6 percent last month.

Productivity is one of the few factors that is both good for both the economy and interest rates. An increase in productivity means more work getting done without a cost increase — good for the economy and also keeping inflation in check.

Unfortunately, we got a decrease in productivity, which has the opposite effect.

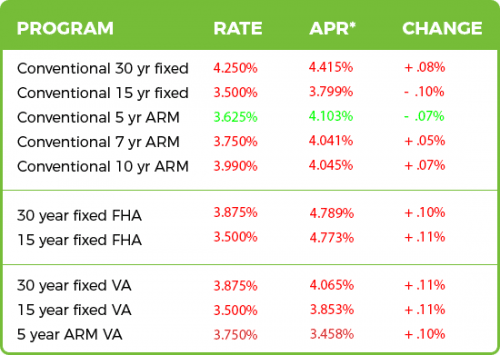

Click to see today’s rates (May 4th, 2017)

Jobs And Orders

Weekly Jobless Claims came in with 7,000 fewer than experts predicted — 238,000 versus 245,000. Fewer jobless claims is slightly positive for the economy and slightly bad for mortgage rates.

Finally, March’s Factory Orders also disappointed — up .2 percent instead of the expected .5 percent. This would be great for mortgage rates, but the report is pretty old, making it less important than last week’s (similar) Durable Goods Report.

Mortgage Rates Today

Tomorrow

There should be plenty of mortgage-relates news stories. Five Fed members are speaking at various engagements today. Market participants will be listening.

The big deal, though, is what we get the first Friday of every month — the Jobs Report. When it varies from expectations, this report can rock the stock and bond markets and cause large mortgage rate changes.

Tomorrow’s report is expected to indicate that the unemployment rate remained at 4.5 percent, that average hourly earnings are up .3 percent, and non-farm payrolls increased almost 100,000 to 190,000.

If actual values indicate a stronger-than-expected economy, rates will rise. If unemployment rose or fewer jobs were created than anticipated, rates could fall.

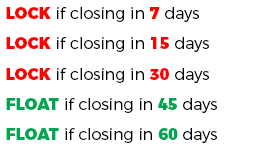

Rate Lock Recommendation

There’s risk of rising rates this week. The Fed is not expected to raise rates, but its post-meeting announcement might offer clues to a rate hike in June. Mortgage rates could rise if anything unexpected is found

What Causes Rates To Rise And Fall?

Mortgage interest rates depend on a great deal on the expectations of investors. Good economic news tends to be bad for interest rates, because an active economy raises concerns about inflation. Inflation causes fixed-income investments like bonds to lose value, and that causes their yields (another way of saying interest rates) to increase.

For example, suppose that two years ago, you bought a $1,000 bond paying five percent interest ($50) each year. (This is called its “coupon rate.”) That’s a pretty good rate today, so lots of investors want to buy it from you. You sell your $1,000 bond for $1,200.

When Rates Fall

The buyer gets the same $50 a year in interest that you were getting. However, because he paid more for the bond, his interest rate is not five percent.

- Your interest rate: $50 annual interest / $1,000 = 5.0%

- Your buyer’s interest rate: $50 annual interest / $1,200 = 4.2%

The buyer gets an interest rate, or yield, of only 4.2 percent. And that’s why, when demand for bonds increases and bond prices go up, interest rates go down.

When Rates Rise

However, when the economy heats up, the potential for inflation makes bonds less appealing. With fewer people wanting to buy bonds, their prices decrease, and then interest rates go up.

Imagine that you have your $1,000 bond, but you can’t sell it for $1,000, because unemployment has dropped and stock prices are soaring. You end up getting $700. The buyer gets the same $50 a year in interest, but the yield looks like this:

- $50 annual interest / $700 = 7.1% The buyer’s interest rate is now slightly more than seven percent.

Click to see today’s rates (May 4th, 2017)

The information contained on The Mortgage Reports website is for informational purposes only and is not an advertisement for products offered by Full Beaker. The views and opinions expressed herein are those of the author and do not reflect the policy or position of Full Beaker, its officers, parent, or affiliates.

Try the Mortgage Calculator

Try the Mortgage Calculatormortgage-rates-today-may-4-2017-plus-lock-recommendations

No comments:

Post a Comment