immigration, irs, greencard, residence, citizenship, social security number, Tax ID number, EIN,employer identification number,legally,aliens,workers,residence,ITIN, [abrir iglesia en los estados unidos], [work from home], [trabaja en los estados unidos]

State National Bank of Big Spring, Texas won’t back down easily.

The bank continues to try and weigh in on the landmark case between PHH and the Consumer Financial Protection Bureau.

Despite motions from other parties being denied, Competitive Enterprise Institute General Counsel Sam Kazman said they are “cautiously optimistic” that their recent motion to intervene will be approved.

The CEI, which advocates for limited government, and the 60 Plus Association, a nonprofit that represents the interests of senior citizens, are also part of the State National Bank case.

“We want to make sure all the constitutional arguments are fleshed out in the PHH case,” said Kazman. “Our plaintiffs wouldn’t be satisfied by the head only being allowed to be removed from the president.”

Under the original PHH ruling, the CFPB authority structure would change and give the president of the United States the power to supervise the director of the CFPB. This would include the ability to replace the director as the president sees fit.

As a refresher, back in 2012, State National Bank filed suit against the federal government, claiming that the CFPB’s “unprecedented, unchecked power” violates the Constitution’s separation of powers.

In August 2013, after 11 states joined State National Bank’s lawsuit, it was tossed by a federal judge, who ruled that the bank did not have standing to sue.

The group didn’t give up and appealed the decision to the U.S. Court of Appeals for the District of Columbia Circuit, eventually winning the appeal in July 2015 when the court ruled the case could move forward.

This is about where the State National Bank case starts to go into limbo and the PHH case starts to begin.

Check here for a more in-depth break down of the timeline.

Younger seniors may be more likely to use a reverse mortgage loan for travel, living expenses or financial planning, while older seniors more often have health care needs, says Meehan.

While those scenarios may be common, there are no restrictions — age-related or otherwise — on how seniors can use reverse mortgage proceeds.

Beth Paterson, certified reverse mortgage loan professional at Reverse Mortgages SIDAC in St. Paul, Minnesota, recalls a 96-year-old borrower who used a reverse mortgage to hit the road.

“She had a $2 million home, condo in Florida and lot of (other) assets, and she was still able to travel, so she did the reverse mortgage instead of tapping into her other retirement funds,” Paterson says.

Understanding a reverse mortgage

No mental competency test or medical exam is required to get a reverse mortgage loan. However, lenders are aware that competency can diminish with age.

Loan officers “should not ignore” any signs of diminished capacity, says Wills, of Open Mortgage. “You have to understand what you are signing.”

Meehan, with Movement Mortgage, asks seniors to recall short-term information while he speaks with them, to get a feel for whether they fully understand. He also may ask older seniors whether a family member or other trusted adviser can review the loan information with them.

In some cases, a guardian, adult child or other trusted financial adviser given power of attorney may be involved in a senior’s reverse mortgage loan.

Wills says a power of attorney must be accompanied by a physician’s letter confirming that the authorization was given when the borrower was mentally competent.

Fulfilling the financial assessment

All reverse mortgage borrowers must complete a financial assessment to help ensure they’ll be able to maintain their home and pay their property taxes and homeowners insurance. This assessment isn’t used to approve or deny a loan, but it may prompt a lender to set aside part of the loan proceeds to pay taxes and insurance on the borrower’s behalf.

The financial assessment may be more challenging for some older seniors.

“Sometimes the older people don’t have part-time jobs but may just be living on Social Security, so sometimes it may be a little bit harder (for them) to qualify under the financial assessment,” Wills says.

But here’s something that can offset a set-aside, if it’s required: Older borrowers can tap a larger percentage of their home’s equity. The reason is that their life expectancy is shorter, meaning the expected term of their loan will be shorter, too.

Berkshire Hathaway CEO Warren Buffett. (Rick Wilking/Reuters)

Billionaire Warren Buffett has some wise words for investors: Stop throwing money away on bad advice.

In his annual letter to shareholders released over the weekend, the Berkshire Hathaway chief executive bashed active fund managers who charge higher fees on the promise that they can do better than the broader market. Buffett said most savers would be better off putting their money in low-cost index funds over the long term, and he estimated that investors wasted roughly $100 billion over the past decade on unnecessary fees.

The “massive fees” charged by active fund managers — who often promise to outperform the broader market — can leave savers worse off than if they had simply used a low-cost index fund that tracks a stock-market index, Buffett warned.

It is never too early to seek help as you prepare for retirement, but picking a financial advisor can be tricky. Here are some tips to consider when searching for the perfect advisor for you. (Ashleigh Joplin,Jonnelle Marte/The Washington Post)

To illustrate his argument, the “Oracle of Omaha” laid out the results of a challenge he presented to fund managers more than a decade ago. In 2005, he bet $500,000 that no investment professional could find five hedge funds that would match the performance of an index fund tracking the Standard & Poor’s 500-stock index over the long run. Only one fund manager stepped up to the plate: Ted Seides, a co-manager of the investment firm Protégé Partners.

Over the first nine years of the challenge, the five hedge funds chosen by Seides delivered an average 2.2. percent a year. The S&P 500 funds picked by Buffett returned an average 7.1 percent a year. “That means $1 million invested in those [hedge] funds would have gained $220,000. The index fund would meanwhile have gained $854,000,” Buffett wrote.

While some of the funds chosen by Seides showed fewer losses than the S&P 500 index fund in some years or gained more than the index in other years, the index fund outshone them all over the long run:

Buffett cites “human behavior” as a reason investors continue to choose costly funds. Some people associate bigger price tags with higher quality, he said, adding that the same isn’t always true when it comes to investing. Many investors, college endowments and pension funds would be better off using the simpler investment products, he wrote, noting that even a 1 percent fee can add up over time.

Last year, the Labor Department finalized the so-called fiduciary rule. The regulation would make it more difficult for some brokers to recommend pricey or complicated investment products and would require brokers working with retirement savers to put their client’s interests ahead of their own. In some cases, that could require brokers who are choosing between two similar funds to recommend the less-expensive option.

Earlier this month President Trump signed a memo asking officials to reevaluate the fiduciary rule and determine if it is harmful to investors, a move that supporters of the regulation fear is an effort to weaken or eliminate the rule altogether.

In the letter, Buffett also praised famed investor John “Jack” Bogle, the founder of Vanguard Group and a pioneer in the index fund universe. “In his early years, Jack was frequently mocked by the investment-management industry,” Buffett wrote. “Today, however, he has the satisfaction of knowing that he helped millions of investors realize far better returns on their savings than they otherwise would have earned.”

Younger seniors may be more likely to use a reverse mortgage loan for travel, living expenses or financial planning, while older seniors more often have health care needs, says Meehan.

While those scenarios may be common, there are no restrictions — age-related or otherwise — on how seniors can use reverse mortgage proceeds.

Beth Paterson, certified reverse mortgage loan professional at Reverse Mortgages SIDAC in St. Paul, Minnesota, recalls a 96-year-old borrower who used a reverse mortgage to hit the road.

“She had a $2 million home, condo in Florida and lot of (other) assets, and she was still able to travel, so she did the reverse mortgage instead of tapping into her other retirement funds,” Paterson says.

Understanding a reverse mortgage

No mental competency test or medical exam is required to get a reverse mortgage loan. However, lenders are aware that competency can diminish with age.

Loan officers “should not ignore” any signs of diminished capacity, says Wills, of Open Mortgage. “You have to understand what you are signing.”

Meehan, with Movement Mortgage, asks seniors to recall short-term information while he speaks with them, to get a feel for whether they fully understand. He also may ask older seniors whether a family member or other trusted adviser can review the loan information with them.

In some cases, a guardian, adult child or other trusted financial adviser given power of attorney may be involved in a senior’s reverse mortgage loan.

Wills says a power of attorney must be accompanied by a physician’s letter confirming that the authorization was given when the borrower was mentally competent.

Fulfilling the financial assessment

All reverse mortgage borrowers must complete a financial assessment to help ensure they’ll be able to maintain their home and pay their property taxes and homeowners insurance. This assessment isn’t used to approve or deny a loan, but it may prompt a lender to set aside part of the loan proceeds to pay taxes and insurance on the borrower’s behalf.

The financial assessment may be more challenging for some older seniors.

“Sometimes the older people don’t have part-time jobs but may just be living on Social Security, so sometimes it may be a little bit harder (for them) to qualify under the financial assessment,” Wills says.

But here’s something that can offset a set-aside, if it’s required: Older borrowers can tap a larger percentage of their home’s equity. The reason is that their life expectancy is shorter, meaning the expected term of their loan will be shorter, too.

Johns Hopkins Medicine said Wednesday it will work with health real estate firm Welltower Inc. to come up with programs and explore developing facilities to serve and treat the elderly.

Welltower develops assisted-living centers, memory care facilities and other medical institutions for the elderly. Company officials said programs and technology developed in those facilities said could be useful to Johns Hopkins, particularly as the trend in health care is to do more treatment outside hospitals.

Welltower properties and programs serve more than 200,000 elderly and accommodate more than16 million patient visits each year.

“This collaboration builds on our shared vision for modern, efficient health care infrastructure,” Mark Shaver, vice president of business development and strategic alliances for Johns Hopkins Medicine, said in a statement. “The changing health care delivery landscape underscores the need for a streamlined healthcare continuum to raise the quality of care, shift care to appropriate, lower-cost settings. and connect caregivers and patients.”

Thomas J. DeRosa, Welltower’s chief executive officer, said in a statement: “Caring for the frail elderly and people with dementia and other diseases of aging present both clinical and economic challenges for health systems. Our collaboration with Johns Hopkins Medicine will advance innovation to keep this at-risk population healthy, socially engaged and out of the high-cost hospital.”

Profits at Mill Valley, Calif.-based Redwood Trust shrank during the fourth quarter, reflecting lower interest income and net losses on the fair value of investments.

• Prepayment speeds (historically a good indicator of refinance activity) declined by 30 percent in January to the lowest level since February 2016

• Delinquencies improved by 3.9 percent from December and were down 17 percent from January 2016

• Foreclosure starts rose 18 percent for the month; January’s 70,400 starts were the most since March 2016

• 2.6 million borrowers are behind on mortgage payments, the lowest number since August 2006, immediately following the pre-crisis national peak in home prices

According to Black Knight’s First Look report for January, the percent of loans delinquent decreased 3.9% in January compared to December, and declined 16.6% year-over-year.

The percent of loans in the foreclosure process declined 0.5% in January and were down 27.6% over the last year.

Black Knight reported the U.S. mortgage delinquency rate (loans 30 or more days past due, but not in foreclosure) was 4.25% in January, down from 4.42% in December.

The percent of loans in the foreclosure process declined in January to 0.94%.

The number of delinquent properties, but not in foreclosure, is down 413,000 properties year-over-year, and the number of properties in the foreclosure process is down 178,000 properties year-over-year.

Black Knight: Percent Loans Delinquent and in Foreclosure Process

Jan

2017

Dec

2016

Jan

2016

Jan

2015

Delinquent

4.25%

4.42%

5.09%

5.48%

In Foreclosure

0.94%

0.95%

1.30%

1.76%

Number of properties:

Number of properties that are delinquent, but not in foreclosure:

2,162,000

2,248,000

2,575,000

2,764,000

Number of properties in foreclosure pre-sale inventory:

Home prices have climbed more than 5% annually for the second straight year, but today’s mortgage rates are still low, and homes are still affordable.

But what will happen through 2017? Likely, a drop in home affordability.

Home prices are expected to keep climbing, and mortgage rates aren’t expected to drop back to the 3s — where they were in mid-2016.

So, what should you do if you’re on the fence about buying?

You might consider buying a home now, but buying too early can be costly, too.

There’s no “right answer”, but one thing’s nearly certain — the best deals you find in housing may be the ones you find today. By this time next year, buying a home could be an expensive proposition.

Each quarter, the National Association of Homebuilders (NAHB) attempts to measure whether U.S. homes are “affordable” for the typical U.S. household.

The group measures median household incomes within 225 metropolitan areas nationwide and — using average 30-year fixed rate mortgage rates — determines whether these incomes can support the typical monthly housing cost.

The index is known as the Home Opportunity Index (HOI).

In last year’s fourth quarter, the Home Opportunity Index hit 59.9%, which means that about six-in-ten homes are affordable to households earning a median income. However, affordability stayed level only because home buyers had locked in rates before they rose post-election.

Now, mortgage rates are climbing, and affordability is threatened. Analysts expect rates to end 2017 considerably higher than they are today.

Home prices are up close to six percent from last year. This affects a buyer’s potential monthly payment; and raises the down payment required to purchase a home.

It can be tough enough to scrape together a down payment — especially for buyers putting 20% down on a home. But, not everyone wants to do that.

Home buyers can choose from among the Conventional 97 and the HomeReady™ home loan, each of which requires three percent down; the FHA loan, which requires 3.5% down; and the VA and USDA loans, which require zero money down.

The Conventional 97 mortgage is mostly used by buyers with better-than-average credit who are purchasing single-family homes to “live in”; and the 3% down HomeReady™ home loan is geared at buyers in lower-income census tracts.

Both programs, however, are limited to $424,100, so buyers in “high-cost cities” should consider either putting five percent down, or a different low-downpayment option.

One such option is the FHA loan, which allows for a downpayment of just 3.5% and allows buyers to finance any home which will be their primary residence, so long as the home is a single-unit (e.g.; a house, a townhome, a condo) or a home of up to 4 units.

FHA loan limits are higher than what’s allowed by the Conventional 97 and HomeReady™, ranging up to $636,150.

Another option for buyers making a small downpayment is no-money-down VA loan. Available to buyers with military experience, the VA Home Loan Guaranty program never charges mortgage insurance and mortgage rates are typically the lowest of all loans available.

Lastly, note that there’s another no-money-down loan — the USDA loan — available to buyers, but the program cannot be used in a “big city” markets. Its use is relegated to buyers in the exurbs and in less densely-populated suburban neighborhoods.

For buyers in search of affordable homes, differentiation must be made for “big markets” and “small markets”.

Small markets are often more affordable than big markets; and homes along East Coast and West Coast are often least affordable.

It should be no surprise, then, that many of the Most Affordable U.S. Housing Markets are spread throughout Ohio and Kentucky.

Last quarter, the country’s most affordable small-ranked city was Fairbanks, Alaska.

95.1 percent of homes in one of the most northern U.S. cities were affordable to families earning the area’s median income of $93,800.

Overall, the Midwest ranked highly for home affordability.

Lansing, Michigan: 89.8 percent affordability

Springfield, Illinois: 89.9 percent affordability

Canton, Ohio: 90.4 percent affordability

On the opposite end of the affordability scale sits San Francisco, dead-last on the list of Most Affordable Cities. Less than 8 percent of median income earners can afford a home, under NAHB’s conditions.

But that’s no surprise. The Bay Area has been ranked the Least Affordable place in the U.S. since the fourth quarter of 2012. Before that, New York City took the title for most expensive city each quarter back to 2008.

Consider More Than Home Prices When Considering A Move

The most surprising point of the NAHB study, however, is the comparison between another California city — San Diego — and what is perceived to be one of the most ridiculously high-priced areas in the country: Honolulu, Hawaii.

But urban Honolulu is twice as affordable as San Diego, according to the report, with 36 percent of homes affordable to median income earners.

The median sales price in Honolulu is $556,000 — not cheap by most measures. But median income rises to the task, coming in near $90,000, and one of the highest income readings on the list.

In San Diego, though, home prices are only slightly lower, at $490,000.

But a median-income family earns just over seventy-three thousand dollars annually.

The comparison of two cities reveals the importance of income when it comes to affordability. Home buyers should not necessarily avoid relocating to an “expensive” city, if their income will justify the move.

Conversely, families should examine earning potential before moving to a “cheap” area.

When thinking about a relocation, the NAHB Housing Opportunity Index just might be the first resource you consider.

What Are Today’s Mortgage Rates?

Home prices are rising and so are national rents. You may not be ready to buy a home today but, by next year, the affordability of homes is expected to be worse.

Get today’s live mortgage rates now. Your social security number is not required to get started, and all quotes come with access to your live mortgage credit scores.

The information contained on The Mortgage Reports website is for informational purposes only and is not an advertisement for products offered by Full Beaker. The views and opinions expressed herein are those of the author and do not reflect the policy or position of Full Beaker, its officers, parent, or affiliates.

Mortgage rates drifted downward in a week in which minutes of the most recent Fed meeting loomed large.

The Federal Reserve dropped the week’s biggest bit of economic news when it released the minutes of its most recent monetary policy meeting. It seemed to hint that the Fed could increase short-term interest rates as early as its next meeting, in mid-March.

“In discussing the outlook for monetary policy over the period ahead, many participants expressed the view that it might be appropriate to raise the Federal funds rate again fairly soon” if employment and inflation continue to rise, the Fed minutes said.

That implies that the central bank remains on track to raise the short-term Federal funds rate three times this year, as it forecast in December. Fed rate hikes don’t always lead to higher mortgage rates. But this time around, the consensus among economists and investors is that Fed rate increases will be accompanied by rising mortgage rates.

Bankrate’s benchmark mortgage rate survey is conducted on Wednesdays, and the data had been collected by the time the Fed minutes were released Wednesday afternoon.

The benchmark 30-year fixed-rate mortgage fell this week to 4.29 percent from 4.35 percent, according to Bankrate’s weekly survey of large lenders. A year ago, it was 3.80 percent. Four weeks ago, the rate was 4.32 percent. The 30-year fixed-rate average for this week is 0.06 percentage points below the 52-week high of 4.35 percent, and is 0.77 percentage points greater than the 52-week low of 3.52 percent.

The 30-year fixed mortgages in this week’s survey had an average total of 0.29 discount and origination points.

Over the past 52 weeks, the 30-year fixed has averaged 3.84 percent. This week’s rate is 0.45 percentage points higher than the 52-week average.

The benchmark 15-year fixed-rate mortgage fell to 3.48 percent from 3.51 percent.

The benchmark 5/1 adjustable-rate mortgage fell to 3.45 percent from 3.51 percent.

The benchmark 30-year fixed-rate jumbo mortgage fell to 4.28 percent from 4.34 percent.

At the current 30-year fixed rate, you’ll pay $494.28 for every $100,000 you borrow, down from $497.81 last week.

At the current 15-year fixed rate, you’ll pay $713.90 for every $100,000 you borrow, down from $715.37 last week.

At the current 5/1 ARM rate, you’ll pay $446.26 for every $100,000 you borrow, down from $449.60 last week.

Weekly national mortgage survey

Results of Bankrate.com’s weekly national survey of large lenders conducted February 22, 2017 and the effect on monthly payments for a $165,000 loan:

As Black History Month observances continue throughout the nation, now is an apt time to revisit the unmet housing finance challenges that affect African-Americans, other consumers of color and low-income whites. While many consumers have felt an economic recovery, many others remain locked out of homeownership and the resulting opportunity to build wealth through home equity.

In order to open up homeownership opportunities to those left behind, public policies must address the impact of mortgage discrimination by promoting robust mortgage lending to all creditworthy borrowers.

An analysis of 2015 Home Mortgage Disclosure Act data by the Center for Responsible Lending found lingering and disturbing disparities. HMDA’s annual report is the nation’s only one that connects race and income with mortgage lending trends.

When it comes to the most affordable home purchase loans, conventional loans remain the least costly for borrowers and the least likely to default. Even so, among the 1,894,000 loans made in 2015, only 2.7% — or 51,202 — conventional home purchase loans were made to African-American borrowers. Latino borrowers fared only slightly higher with 5.1% of these loans, or 96,975. These figures stand in stark contrast to the 1,361,564 conventional loans made to non-Hispanic, white borrowers, representing over 72%.

That same year, Federal Housing Administration lending provided a well-utilized option for 765,880 non-Hispanic white borrowers accounting for 62% of these loans. Participation by borrowers of color, however, was still meager. Over 13% of FHA loans went to Latino borrowers (162,317), and fewer than 10% to African-Americans (120,618).

It is also noteworthy that, without regard to ethnicity, low-down-payment FHA loans were accessed by over 460,000 low-and moderate- income borrowers.

Owning a home is the cornerstone of the American dream. But it is a dream rooted in a history of inequity. For decades, federal housing policy fostered discrimination in mortgage lending in communities of color that hindered families from safely joining the ranks of America’s growing middle class. From Jim Crow to post-World War II, white homeownership served as a foundation to building wealth that transferred in later years to younger generations.

As a result, families of color have much less wealth than comparable whites. According to the Survey of Consumer Finances, whites have 10-times the wealth of Latinos, and 12-times the wealth of African-Americans.

Predatory lending dominated formerly redlined communities and, again, borrowers of color were negatively impacted. CRL research on the effects of subprime lending found that a disproportionate number of foreclosures occurred in communities of color — even when these borrowers qualified for less expensive and sustainable mortgage loans. When nearly 5 million families lost their homes to foreclosure, the brunt of financial losses were borne by those who had the least wealth: consumers of color. The post-foreclosure spillover costs for these consumers totaled $1 trillion.

Yet, borrowers who received safe mortgages without risky features performed much better. A report on Self-Help Credit Union’s Community Advantage Program, from the University of North Carolina’s Center for Community Capital, showed that those borrowers amassed a net worth of $38,000 compared to renters’ $266, even as housing values plunged. The Community Advantage Program securitized mortgages for more than 50,000 families in 48 states.

Dodd-Frank, and by extension the Consumer Financial Protection Bureau, includes mortgage protections that prohibit many of the risky practices that fueled the mortgage meltdown. These sensible protections established the ability-to-repay standard on all mortgage loans, along with bright line rules that safeguard consumers and lenders alike.

Instead of being encouraged by the reforms in the housing finance system, conventional mortgage lenders instituted market overcorrections that prevent creditworthy borrowers from accessing mortgage loans. The Urban Institute reported that 4 million potential borrowers were locked out of the mortgage market from 2009 to 2013 due to unnecessarily tight credit standards as most loans were to borrowers with high credit profiles. Urban also showed that white borrowers received more mortgages due to their higher credit profiles.

The Federal Housing Finance Agency made recent strides in this direction by once again allowing Fannie Mae and Freddie Mac to secure mortgages with smaller down payments.

While this is a step in the right direction, it is not enough. FHFA must reverse its trend towards risk-based pricing in its loan guarantee fees and loan-level price adjustments. It also should prevent risk-based pricing in front-end credit risk transfers, including deeper mortgage insurance. Pricing structures are important, as they can incentivize lending that only serves those with the least risky credit profiles.

Instead, our system should continue to pool credit risk. This would encourage conventional lenders to make loans to potential mortgage buyers of color and low-income whites, ensuring that all creditworthy families have access to their American dreams.

Nikitra Bailey is an executive vice president with the Center for Responsible Lending.

Garmin Ltd. (GRMN) beat EPS and revenue estimates while issuing inline fiscal year 2017 guidance in their fourth-quarter earnings report on Wednesday morning. The news triggered a strong buy-the-news reaction, lifting the stock to a 6-month high that should presage even stronger gains in coming weeks. The rally could even mark the next phase of a larger-scale recovery that finally brings the 2007 high in triple digits into view.

The GPS giant got booted from the Nasdaq-100 index in 2015 and has fallen off the trading screens of many market players since that time. However, the keepers of the tech-heavy index could eventually regret their decision because the company now sports a market cap close to $10-billion while engaged in a major comeback that could open the door to dramatic investor returns.

GRMN Long-Term Chart (2000-2017)

The company came public near $10 (post one stock split) in December 2000, right in the middle of the Dot-com bear market, and traded sideways in a 7-point range into a December 2002 breakout. The subsequent uptrend continued into the December 2003 high at $29.74 and gave way to a brutal decline that relinquished more than half of the stock‘s value, coming to rest at $14.04. Keep that level in mind because it came back into play during the 2008 economic collapse.

A recovery wave reached the 2003 high at the end of 2004, giving way to a 2005 breakout that generated substantial momentum, starting in 2006. That rally entered a parabolic phase in June 2007, more than doubling in price into the October 2007 all-time high at $125.68. Aggressive sellers then took control, generating a broken bubble that found support at the 2004 low in the upper teens in November 2008.

A bounce into the second half of 2009 confirmed severe technical damage, failing to pierce the 25% retracement of the triple digit decline. The stock then settled into a sideways pattern that took more than two years to clear that minor barrier, ahead of a 2012 breakout that failed to hold new support. Sellers took control once again, dropping the stock into the lower-30s, ahead of a larger-scale recovery wave that topped out at a 6-year high in July 2014.

Choppy two-sided price action has continued into 2017, with a 4-year low in January 2016, followed by a strong bounce that’s now reached the .786 retracement of the 2014 into 2016 downtrend. Rally waves between 2009 and 2014 have generated a rising highs trendline, with resistance now centered in the low-70s, at the 50% bear market retracement. This price zone marks a logical target if the stock continues its upward trajectory.

GRMN Short-Term Chart (2015–2017)

A major decline found support in the low-30s at the start of 2016, giving way to a recovery wave that reached the .786 Fibonacci retracement level in August. It pulled back to the 200-day EMA earlier this month and turned higher into earnings, with the initial reaction generating a rally into 2016 resistance at $55. A breakout above this level should complete a 100% round trip into the 2014 high in the lower-60s, ahead of a continued upside into the rising highs trendline.

On Balance Volume (OBV) topped out at a multi-year high in 2014 and ground sideways into the middle of 2015. It then entered an aggressive distribution wave, dumping to a 3-year low in the first-quarter of 2016. Buying interest then perked up, generating a modest uptick that’s now lifted into 2015 levels. This proportional activity matches price action perfectly, pointing to a technical healing process that should continue into coming months.

The Bottom Line

Garmin has been on the recovery trail for the last 13 months and could now break out above the 2016 high in the mid-50s. The next upside target lies at the 2014 high in the low-60s, with that level likely to give way and yield a final buying surge into the low-70s.

<Disclosure: the author held no positions in aforementioned stocks at the time of publication.>

The Mortgage Bankers Association (MBA) released its weekly report on mortgage applications Wednesday morning, noting a decrease of 2% in the group’s seasonally adjusted composite index for the week ending February 17. During the week, mortgage loan rates increased on all four types of fixed-rate loans and decreased on adjustable rate mortgages.

On an unadjusted basis, the composite index increased by 1% week over week. The seasonally adjusted purchase index decreased by 3% compared with the week ended February 10. The unadjusted purchase index increased by 2% for the week and is now 10% higher year over year.

The MBA’s refinance index decreased by 1% week over week, and the percentage of all new applications that were seeking refinancing slipped from 46.9% to 46.2%, its lowest level since November of 2008.

Adjustable rate mortgage loans accounted for 7.3% of all applications, down from 7.5% in the prior week.

Mortgage News Daily commented on the relatively narrow range in which interest rates have moved since last November:

The outright numbers are less important here. They can vary quite a bit based on multiple variables. The fact that rates have been sideways for so long is more relevant. In fact, rates haven’t merely been sideways. The range has been growing progressively more narrow over the past several months.

While this type of “consolidation” is not uncommon in the wake of big market movement, it does mean that rates will soon be forced to choose a direction. Such breakouts tend to see extra momentum. In other words, we’re increasingly due for a bigger move. If you roll the dice on that move being toward lower rates, there’s additional reward for that risk. For most borrowers, however, that potential for reward is overshadowed by the increased risk of a big move toward higher rates.

According to the MBA, last week’s average mortgage loan rate for a conforming 30-year fixed-rate mortgage increased from 4.32% to 4.36%. The rate for a jumbo 30-year fixed-rate mortgage rose from 4.28% to 4.29%. The average interest rate for a 15-year fixed-rate mortgage rose from 3.55% to 3.56%.

The contract interest rate for a 5/1 adjustable rate mortgage loan decreased from 3.34% to 3.31%. Rates on a 30-year FHA-backed fixed-rate loan increased from 4.12% to 4.14%.

If you are shopping for a mortgage, you have probably seen all sorts of offers and advertisements aimed at first-time home buyers and wondered if these are really as good as they sound. In some cases, “first-time” programs are little more than attention getting marketing messages from lenders, while in others they are actual assistance programs for people who may otherwise face challenges with qualifying for a home mortgage or finding a home loan at an affordable interest rate. With this in mind, it is important to understand the difference between mortgage lender marketing programs, actual loan programs, and financial assistance programs.

You can be a first-time home buyer more than once

First of all, even if you have previously owned a home, you (or your spouse) may still qualify as a first-time home buyer. According to the U.S. Department of Housing and Urban Development, first-time home buyer status is not limited to people who have never owned a home before (although that criteria obviously applies). For lending purposes, a first-time home buyer includes anyone who fits one or more of these conditions:

An individual or a spouse who has not owned a primary residence for at least three years. This means married couples may qualify as first-time buyers even if only one of them meets this test.

A single parent who previously only owned a home with a spouse while they were married.

Someone who has only owned a primary residence that was not attached to a permanent foundation (e.g., a mobile home) in accordance with applicable regulations.

Displaced homemakers whose only previous ownership was with a spouse.

Someone who only owned property that was not in compliance with local building code ordinances and which cannot be improved to meet building code standards for less than the cost of constructing a new residence.

Types of programs

First-time home buyer programs can be broadly categorized as either loan programs or financial assistance programs. Both types of programs can be helpful to first-time home buyers. Loan programs, such as those backed by the Federal Housing Administration (FHA), are available to all borrowers through various commercial lenders, but they have features that may be particularly attractive to first-time buyers with lower credit scores or little in the way of cash savings. Private lenders may also offer attractive loan rates and terms for first-time home buyers with good credit and the ability to make larger down payments on a home purchase. Financial support programs for home buyers typically come from state and local government entities, although the federal government sometimes steps in to provide additional assistance during difficult economic times.

Loan programs

Mortgage loans are made by commercial lenders, such as banks, credit unions, or mortgage companies. These loans may be guaranteed by various organizations, both to protect lenders against borrower defaults and also to make loans more affordable for borrowers.

FHA. The Federal Housing Administration does not make loans, although they do insure loans made by commercial lenders to protect lenders if borrowers default on loan payments. FHA loans are available to all qualified buyers, and they can be particularly attractive to first-time home buyers because the qualifications are easier. For example, a potential home buyer with a credit score of at least 580 may qualify for an FHA loan with as little as 3.5% of the purchase price for a down payment. Lower credit scores between 500 – 579 may also qualify with a larger down payment of 10%, though the interest rate on the mortgage loan will be higher.

VA. The Veteran’s Administration (VA) also guarantees portions of home loans provided by private banks or mortgage companies to active duty service members, veterans, and eligible surviving spouses. A home purchase loan guaranteed by the VA can help military vets and spouses purchase homes at competitive interest rates without the need to also make a down payment or purchase private mortgage insurance. Applicants must have satisfactory credit scores, along with sufficient income to meet expected monthly loan payments.

USDA Single Family Housing Guaranteed Loan Program. Similar to loan programs provided by FHA and VA, the United States Department of Agriculture (USDA) also provides loan guarantees to mortgage lenders so they can help borrowers with low and moderate incomes purchase homes in rural areas. The USDA program guarantees 90% of mortgage loan amounts for approved lenders to help offset the risk of offering 100% loans to eligible rural home buyers.

Freddie Mac Home Possible® Mortgages. The Federal Home Loan Mortgage Corporation (also known as “Freddie Mac”) makes it possible for lenders to offer home loans to buyers with down payments as small as 3% through the Home Possible® Although this program is not limited only to first-time home buyers, first-timers must first participate in a borrower education program.

Home Buying Financial Assistance

Financial assistance programs exist across all levels of government: city, state, and federal. These programs may provide assistance with funds for down payments, closing costs, or other expenses tied to the home purchase process.

Fannie Mae’s HomePath Ready Buyer Program. In 2015 the Federal National Mortgage Association (FNMA or “Fannie Mae”) launched the HomePath Ready Buyer program, which provides first-time home buyers up to 3% of the home’s purchase price in the form of a rebate to assist with closing costs. Participants must complete an online home buyer education course in order to receive the 3% rebate.

State-by-state home buyer programs. Many individual states sponsor a variety of home buyer programs designed to help first-time home buyers and others qualify for home mortgages. Visit your state’s housing website to find details for your area. For example, first-time home buyers with low or moderate incomes are eligible for the Texas Mortgage Credit Certificate Program as a way to convert mortgage interest into a federal income tax credit. New York state home buyers can take advantage of the Conventional Plus Program for down-payment assistance up to 3% of the home’s purchase price.

City & county home buyer programs. Individual cities and municipalities can also offer assistance with home financing. For example, Miami/Dade County in Florida makes home financing assistance available to first-time home buyers through a loan program facilitated between Miami-Dade County Public Housing and Community Development and local mortgage lenders. Similarly, the Mayor’s Office of Housing and Community Development in San Francisco provides loan assistance programs for first-time home buyers. Consult with your city or county government offices for availability of similar programs.

As you review and evaluate the financial assistance or loan programs that may be a good fit for you, it is also a good idea to take inventory of your personal financial situation, such as checking your credit report (www.annualcreditreport.com), paying off credit cards and personal loans, and stashing more cash into your emergency fund. These tips and more are also available in this article: 5 Steps to Buying a Home.

Here are some excerpts from a post I wrote in February 2005 (hard to believe this was 12 years ago).

Note: I think I’ve improved the graphs since then! From 2005:

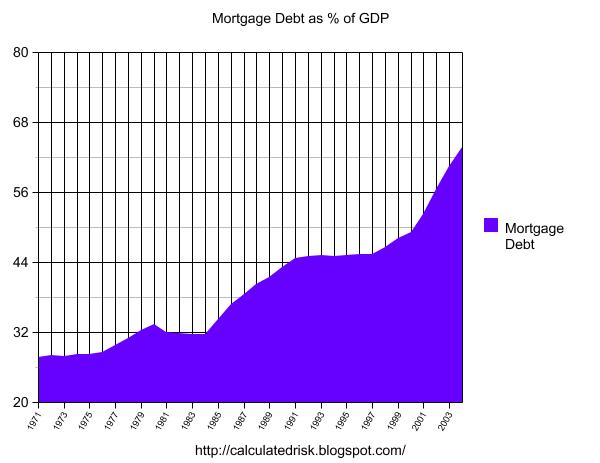

The following chart shows household mortgage debt as a % of GDP. Although mortgage debt has been increasing for years, the last four years have seen a tremendous increase in debt. Last year alone mortgage debt increased close to $800 Billion – almost 7% of GDP.

Source: Federal Reserve

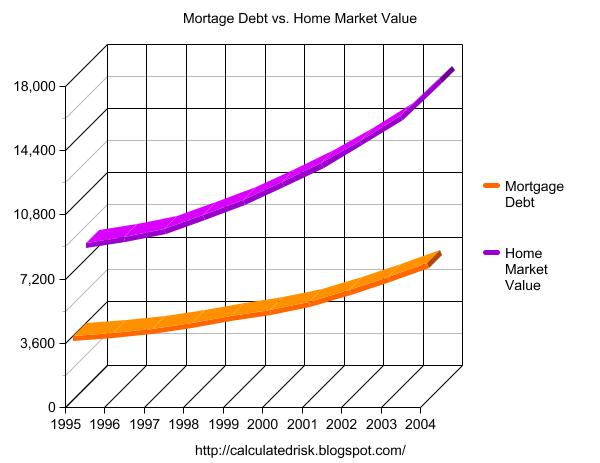

Some obervers have remarked that mortgage debt is still below 50% of household RE assets – and that is an accurate statement. In fact, if you plot mortgage debt vs. household RE assets everything looks reasonable.

Source: Federal Reserve

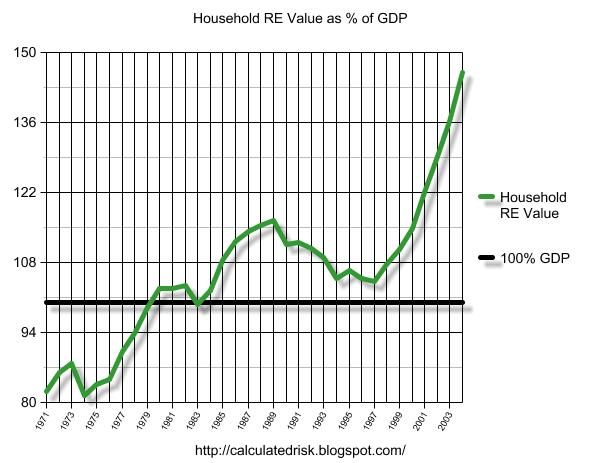

But lets plot household RE assets as a % of GDP.

Source: Federal Reserve

This final graph shows the potential problem. Household assets have really soared in the last few years. Many homeowners have refinanced their homes (or moved and taken cash out), in essence using their homes as an ATM.

It wouldn’t take a RE bust to impact the general economy. Just a slowdown in both volume (to impact employment) and in prices (to slow down borrowing) might push the general economy into recession. An actual bust, especially with all of the extensive sub-prime lending, might cause a serious problem.

Until recently, Timothy and his wife Brenda, along with their three children, had been life-long renters.

They did not rent simply because they enjoyed renting. They rented because Brenda was a stay-at-home mom, and with just one income.

Their budget didn’t extend far enough to cover their monthly bills.

As a result, there were times where they were forced to live off of their credit cards. A couple of late payments and a few maxed out credit cards took a toll on their credit scores.

Tim’s credit score was 577. His bank turned him down due to his less-than-perfect FICO.

Fortunately, thanks to a lender’s credit analyzer program, Tim was able to get a detailed game plan on how to get his credit scores up.

Eager to become homeowners, Tim and Brenda followed the instructions to the “T”. All they had to do was pay down a couple of credit cards, and transfer a balance from one card to another. The cost to do this: just under $500.

With the help of a rapid rescore, they saw immediate results. In less than one week, Tim saw his credit score jump almost 50 points!

With Tim’s credit score now at 625, Tim and Brenda went home shopping that very weekend. They found their dream home, made an offer, and moved into their new home just 30 days later.

College Student Gets A Home, Parents Start Investment Portfolio

Jennifer is starting college in the fall. It is both an exciting and anxious time for her as this will be her first time living on her own, away from home.

She applied for a mortgage but was told she didn’t qualify due to her lack of income and employment. Unfortunately, her part-time income from her new job wasn’t enough to get her approved for a home loan.

Jennifer and her parents met with a lender to discuss some options. Initially, her parents were considering co-signing for their daughter.

However, after exploring some of the parent’s long-term financial goals, another option surfaced.

Jennifer’s parents had always wanted to invest in real estate. However, they were apprehensive about being landlords.

The parents were also unsure as to how much they would need for a down payment, assuming 20-25% would be required. They had some money in savings, but they didn’t want to empty their nest egg.

A 25 percent down payment just wasn’t feasible. 20 percent was possible but it would deplete their savings.

Fortunately, after meeting with their lender, Jennifer’s parents were pleasantly surprised to learn that only 15% was needed for down payment.

Jennifer not only gets to live in a new home as she starts college, but her parents are venturing into real estate investing, on their terms and at their pace.

Tired Of Paying FHA Mortgage Insurance

FHA loans are great, especially for buyers like Daniel, who bought his first home five years ago.

Daniel was initially turned down when he applied for a conventional loan.

Not only did he have less-than-perfect credit, he had limited funds for down payment. With FHA’s relaxed credit guidelines, as well as the small down payment requirement of just 3.5 percent, an FHA loan was perfect at the time.

Now, five years later, thanks to a thriving real estate economy, Daniel’s home has appreciated significantly.

According to CoreLogic, U.S. home prices have appreciated about 6 percent over the past few years.

He refinanced out of his FHA mortgage and into a conventional loan. Now that he had better credit scores — a byproduct of owning a home and making on-time payments — he also dropped his interest rate by 0.25%.

Thanks to a lower rate and no mortgage insurance, the refinance saved Daniel $235 per month.

Daniel’s plan is to take that $235 savings and apply it right back towards the principal of his new loan.

In doing so, Daniel will be able to pay off his 30-year loan in just 21 years.

Some homeowners in Daniel’s situation may be reluctant to refinance back out to a 30-year term for fear that they are throwing away those five years of payments that were already made.

However, using Daniel’s example, instead of going backwards, Daniel is actually cutting four years off of his term. Not to mention the increased tax benefits now that Daniel is back to paying more interest now that his new loan is re-amortized.

What Are Today’s Mortgage Rates?

Being denied by one lender doesn’t mean you’ll be denied by every lender. There may be a number of loan programs available that may fit your situation. You just don’t know about them yet.

Don’t give up just because you’ve been turned down. Try, try again.

The information contained on The Mortgage Reports website is for informational purposes only and is not an advertisement for products offered by Full Beaker. The views and opinions expressed herein are those of the author and do not reflect the policy or position of Full Beaker, its officers, parent, or affiliates.

If you are shopping for a mortgage, you have probably seen all sorts of offers and advertisements aimed at first-time home buyers and wondered if these are really as good as they sound. In some cases, “first-time” programs are little more than attention getting marketing messages from lenders, while in others they are actual assistance programs for people who may otherwise face challenges with qualifying for a home mortgage or finding a home loan at an affordable interest rate. With this in mind, it is important to understand the difference between mortgage lender marketing programs, actual loan programs, and financial assistance programs.

You can be a first-time home buyer more than once

First of all, even if you have previously owned a home, you (or your spouse) may still qualify as a first-time home buyer. According to the U.S. Department of Housing and Urban Development, first-time home buyer status is not limited to people who have never owned a home before (although that criteria obviously applies). For lending purposes, a first-time home buyer includes anyone who fits one or more of these conditions:

An individual or a spouse who has not owned a primary residence for at least three years. This means married couples may qualify as first-time buyers even if only one of them meets this test.

A single parent who previously only owned a home with a spouse while they were married.

Someone who has only owned a primary residence that was not attached to a permanent foundation (e.g., a mobile home) in accordance with applicable regulations.

Displaced homemakers whose only previous ownership was with a spouse.

Someone who only owned property that was not in compliance with local building code ordinances and which cannot be improved to meet building code standards for less than the cost of constructing a new residence.

Types of programs

First-time home buyer programs can be broadly categorized as either loan programs or financial assistance programs. Both types of programs can be helpful to first-time home buyers. Loan programs, such as those backed by the Federal Housing Administration (FHA), are available to all borrowers through various commercial lenders, but they have features that may be particularly attractive to first-time buyers with lower credit scores or little in the way of cash savings. Private lenders may also offer attractive loan rates and terms for first-time home buyers with good credit and the ability to make larger down payments on a home purchase. Financial support programs for home buyers typically come from state and local government entities, although the federal government sometimes steps in to provide additional assistance during difficult economic times.

Loan programs

Mortgage loans are made by commercial lenders, such as banks, credit unions, or mortgage companies. These loans may be guaranteed by various organizations, both to protect lenders against borrower defaults and also to make loans more affordable for borrowers.

FHA. The Federal Housing Administration does not make loans, although they do insure loans made by commercial lenders to protect lenders if borrowers default on loan payments. FHA loans are available to all qualified buyers, and they can be particularly attractive to first-time home buyers because the qualifications are easier. For example, a potential home buyer with a credit score of at least 580 may qualify for an FHA loan with as little as 3.5% of the purchase price for a down payment. Lower credit scores between 500 – 579 may also qualify with a larger down payment of 10%, though the interest rate on the mortgage loan will be higher.

VA. The Veteran’s Administration (VA) also guarantees portions of home loans provided by private banks or mortgage companies to active duty service members, veterans, and eligible surviving spouses. A home purchase loan guaranteed by the VA can help military vets and spouses purchase homes at competitive interest rates without the need to also make a down payment or purchase private mortgage insurance. Applicants must have satisfactory credit scores, along with sufficient income to meet expected monthly loan payments.

USDA Single Family Housing Guaranteed Loan Program. Similar to loan programs provided by FHA and VA, the United States Department of Agriculture (USDA) also provides loan guarantees to mortgage lenders so they can help borrowers with low and moderate incomes purchase homes in rural areas. The USDA program guarantees 90% of mortgage loan amounts for approved lenders to help offset the risk of offering 100% loans to eligible rural home buyers.

Freddie Mac Home Possible® Mortgages. The Federal Home Loan Mortgage Corporation (also known as “Freddie Mac”) makes it possible for lenders to offer home loans to buyers with down payments as small as 3% through the Home Possible® Although this program is not limited only to first-time home buyers, first-timers must first participate in a borrower education program.

Home Buying Financial Assistance

Financial assistance programs exist across all levels of government: city, state, and federal. These programs may provide assistance with funds for down payments, closing costs, or other expenses tied to the home purchase process.

Fannie Mae’s HomePath Ready Buyer Program. In 2015 the Federal National Mortgage Association (FNMA or “Fannie Mae”) launched the HomePath Ready Buyer program, which provides first-time home buyers up to 3% of the home’s purchase price in the form of a rebate to assist with closing costs. Participants must complete an online home buyer education course in order to receive the 3% rebate.

State-by-state home buyer programs. Many individual states sponsor a variety of home buyer programs designed to help first-time home buyers and others qualify for home mortgages. Visit your state’s housing website to find details for your area. For example, first-time home buyers with low or moderate incomes are eligible for the Texas Mortgage Credit Certificate Program as a way to convert mortgage interest into a federal income tax credit. New York state home buyers can take advantage of the Conventional Plus Program for down-payment assistance up to 3% of the home’s purchase price.

City & county home buyer programs. Individual cities and municipalities can also offer assistance with home financing. For example, Miami/Dade County in Florida makes home financing assistance available to first-time home buyers through a loan program facilitated between Miami-Dade County Public Housing and Community Development and local mortgage lenders. Similarly, the Mayor’s Office of Housing and Community Development in San Francisco provides loan assistance programs for first-time home buyers. Consult with your city or county government offices for availability of similar programs.

As you review and evaluate the financial assistance or loan programs that may be a good fit for you, it is also a good idea to take inventory of your personal financial situation, such as checking your credit report (www.annualcreditreport.com), paying off credit cards and personal loans, and stashing more cash into your emergency fund. These tips and more are also available in this article: 5 Steps to Buying a Home.

Washington Real Estate Investment Trust (NYSE:WRE)

Q4 2016 Earnings Conference Call

February 17, 2017 11:00 ET

Executives

Paul McDermott – President and Chief Executive Officer

Tejal Engman – Director, Investor Relations

Steve Riffee – Executive Vice President and Chief Financial Officer

Tom Bakke – Executive Vice President and Chief Operating Officer

Drew Hammond – Vice President, Chief Accounting Officer and Controller

Kelly Shiflett – Vice President, Finance and Treasurer

Analysts

Dave Rodgers – Robert W. Baird

Chris Lucas – Capital One Securities

Operator

Welcome to the Washington Real Estate Investment Trust Year End 2016 Earnings Conference Call. As a reminder, today’s call is being recorded. Before turning over the call to the company’s President and Chief Executive Officer, Paul McDermott, Tejal Engman, Director of Investor Relations, will provide some introductory information. Ms. Engman, please go ahead.

Tejal Engman

Thank you and good morning everyone. Please note that our conference call today will contain financial measures, such as FFO, core FFO, NOI, core FAD, and adjusted EBITDA that are non-GAAP measures as defined in Reg G. Please refer to our most recent financial supplement and to our earnings press release both available on the Investor page of our website and to our periodic reports furnished or filed with the SEC for definitions and further information regarding our use of these non-GAAP financial measures and the reconciliation of them to our GAAP results.

Please also note that some statements during this call are forward-looking statements within the Private Securities Litigation Reform Act. Forward-looking statements in the earnings press release along with our remarks are made as of today and we undertake no duty to update them as actual events unfold. Such statements involve known and unknown risks, uncertainties and other factors that may cause actual results to differ materially. We provide these risks in our SEC filings. Please refer to Pages 9 through 24 of our Form 10-K for our complete risk factor disclosure.

Participating in today’s call with me will be Paul McDermott, President and Chief Executive Officer; Steve Riffee, Executive Vice President and Chief Financial Officer; Tom Bakke, Executive Vice President and Chief Operating Officer; Drew Hammond, Vice President, Chief Accounting Officer and Controller; and Kelly Shiflett, Vice President, Finance and Treasurer.

Now, I would like to turn the call over to Paul.

Paul McDermott

Thank you, Tejal and good morning everyone. Thanks for joining us on our year end 2016 earnings conference call. Washington REIT reported 2016 core FFO of $1.76, which is the midpoint of our guidance range and $0.05 higher than our full year 2015 core FFO of $1.71. Better than expected same-store NOI growth was the key performance driver in 2016. As we grew same-store physical occupancy by 220 basis points while simultaneously growing same-store rents by 160 basis points over full year 2015.

Let me begin by summarizing our successful execution in 2016 and its expected impact on our future growth. Overall, 2016 was a transformational year for Washington REIT. We sold our suburban Maryland office portfolio, reallocated capital into value-add, metro-centric multifamily and further reduced our debt thereby strengthening both the left and right sides of our balance sheet. Our capital allocation elevated the quality of our portfolio, reduced the volatility of our cash flow and improved our net debt to adjusted EBITDA ratio from approximately 7x at year end 2015 to 6.1x at year end 2016.

In aggregate, we believe our execution has improved Washington REIT’s long-term risk-adjusted growth profile. It has also better positioned our portfolio to capitalize on growth opportunities in our region, which remain concentrated in urban, metro-centric locations with walkable amenities. Finally, with our 2016 execution, we have completed our programmatic asset recycling and established a solid platform for our future growth.

Today, we forecast that our portfolio will grow same-store NOI by 4.75% to 5.25% in 2017. This is our highest forecast for annual same-store NOI growth in 5 years or since sequestration impacted the real estate fundamentals in our region. By successfully executing our strategic plan, we have adapted to thrive despite a challenging market and are poised to further benefit from a regional recovery.

Let me now delve into more detailed update on our three portfolios and our six key NOI growth drivers. Starting with office, which contributed 48% of our fourth quarter NOI, we feel optimistic about our portfolio as reflected in our strong 2017 same-store office NOI growth guidance of 7% to 7.5%, primarily driven by positive leasing execution. We believe demand in our region is accelerating. For example, we currently have over 770,000 square feet of tenants that we are touring or trading proposals with and another 1.1 million square feet of prospects for our approximately 285,000 square feet of vacant space at year end 2016. For space that is rolling in 2017, our current prospect pool represents approximately 3x the amount of space available.

Let us now discuss the Army Navy Building, which is one of our near-term NOI growth drivers in office. We have approximately 50,000 square feet of space to lease up at this boutique, trophy asset located in the epicenter of the CBD, overlooking a park and flanked by two major metro stops. We continue to make good progress on the renovations, investing approximately $4 million in total and expect to generate additional stabilized annualized NOI of approximately $2 million above 2016 NOI. Our leasing activity has been strong thus far, especially for small to midsized tenants and continues to validate our pro forma underwriting expectations.

Now, let me address all of our large office lease expirations from 2017 until 2020. I am pleased to report that we have executed a 16-year renewal of one of our 10 largest tenants Hughes Hubbard & Reed. HHR is an A-List law firm at 1775 Eye Street whose approximately 53,000 square foot lease was set to expire in February 2018. We signed an early blend and extend with the tenant at strong gap rents. The fact that a highly coveted tenant like HHR chose to stay with us and renovate in place speaks to the strength of the Washington REIT brand and the value we offer CBD tenants in the form of well located assets with operational expertise at competitive rates.

Furthermore, we are in active negotiations with a significant new tenant to replace Engility’s lease that expires in September 2017 at Braddock Metro Center. Following the company’s recent sale of its USAID business known as the International Resources Group, Engility’s Braddock operations will be consolidating with the acquirer’s current facility. We have developed a comprehensive repositioning plan for the asset, while proactively marketing Engility’s space and have seen excellent activity due to its metro-centric location.

Finally, regarding 2445 M Street, where the Advisory Board is expected to vacate in mid-2019, our immediate focus is to aggressively pursue the office leasing opportunity while continuing to evaluate long-term value creation options. We have hired an industry leading architect and leasing team, which are actively marketing the space as we explore renovating and retenanting the assets in a value-enhancing manner. Situated at the corner of 25th and M Street with an easy walking and biking distance from Foggy Bottom and DuPont Circle Metro locations, this building enjoys the most desirable location in the West End. It is surrounded by popular restaurants, exciting new retail and the city’s top hotels, including the Ritz-Carlton, Four Seasons, Fairmont and Park Hyatt.

We are bullish on the West End submarket, which is historically DC’s tightest office market, with an average direct vacancy rate of 7.4% since 2001. The West End enjoys immediate proximity to key demand drivers, including foreign delegations, embassies and three of DC’s largest employers and influencers: the World Bank, the International Finance Corporation and George Washington University and Hospital. We continue to implement a focused tenant retention program that has proven successful with the recent renewals of large tenants such as the World Bank, Booz Allen Hamilton, Epstein, Becker & Green, and now Hughes Hubbard & Reed. That said our diversified office portfolio as a whole caters more to small and midsized tenants than it does to large tenants. In 2016, our average office deal was approximately 5,600 square feet, which reflects the average deal size for our market and where the highest level of tenant activity occurs. Our office NOI remains fairly evenly split between the district and Northern Virginia and we see secular growth drivers for both markets. As mentioned on our last call, in the district, we continue to observe that the availability of well located office space priced at the mid-$40 to mid-$50 gross rent is limited. We continue to see good, steady tenant activity in this price range with both concessions and vacancy rates improving as supply is removed to be repositioned into trophy office space priced in the mid to high-$70 per foot. All of our district office assets are in excellent locations with the majority offering rents in this pricing sweet spot. Washington REIT continues to seek value add opportunities that fits this profile.

In Northern Virginia, we continue to see office leasing concentrated in metro accessible locations and continue to benefit from the fact that all of our office assets with the exception of one are proximate to strong transportation links, including metro. In the aftermath of the election, Northern Virginia is poised to benefit from a potential increase in federal dispense related spending, which is expected to lead to defense contractor expansion. This tenant constituency has downsized significantly following the onset of sequestration and currently has very little shadow space. Approximately 15% of our overall office portfolio is currently occupied by defense contractors. We expect both our Northern Virginia office and multifamily portfolios to benefit from their anticipated increase in office net absorption in the region.

Moving on to multifamily, which contributed approximately 28% of our fourth quarter NOI, the trends in net effective renewals and new leases are improving both on a month-over-month and a year-over-year basis. Despite continued record levels of new supply in 2016, we were able to increase both rents and occupancy for approximately half of our same-store multifamily portfolio on a year-over-year basis versus none in 2015 over 2014. Our same-store multifamily rents have slowly, but steadily accelerated on a year-over-year basis in every quarter of 2016, from negative 30 basis points in the first quarter to positive 80 basis points in the fourth quarter. We benefit from having a multifamily portfolio that is predominately composed of well located B to B+ assets, which are relatively less impacted by an increase in supply as composed of significantly more expensive Class A product.

In the Washington Metro region, almost a quarter of households earning greater than $45,000 a year are defined as being housing burdened, given they spend more than 30% of their income on housing. As per this measure, the proportion of housing burdened renters in our market is higher than in every major market in the country with the exception of LA, San Jose and San Diego. We therefore continue to see a flight to value driven by value conscious renters seeking affordable, well located product. We further benefit from having the majority of our portfolio located in submarkets within Northern Virginia that are not directly competing with the largest wave of Class A deliveries in specific submarkets in the district, such as the Ballpark in Southeast D.C. In our region, Class B multifamily assets outperformed Class A, both in terms of net effective rent growth and occupancy in the fourth quarter of 2016. As per Real Page, fourth quarter Class B net effective rents grew 100 basis points faster than Class A net effective rents, while Class B vacancy was 20 basis points lower than Class A vacancy.

Overall, the outlook for multifamily is steadily improving as absorption remained strong, while new supply has declined by 14% in the fourth quarter of 2016 on a year-over-year basis. Our near-term NOI growth drivers in multifamily are the unit renovation programs at The Wellington and Riverside Apartments where we are renovating units as they turnover. Both assets are located in submarkets with a significantly greater than average affordability gap between Class A and B monthly rents. As of December 2016, 219 out of 680 planned units have been renovated at The Wellington and 100 out of 850 planned units have been renovated at Riverside Apartments. We have been able to generate mid to high teens return on costs on the renovation dollars that have been invested at these two assets to-date.

We continue to expect to generate incremental annual NOI of approximately $4 million above 2016 NOI, following the completion of the entire renovation program. We expect to spend a combined total of approximately $23 million on unit renovations at both assets from the inception of the program through the end of 2018. Furthermore, we are currently preparing the site at The Wellington for the ground-up development of approximately 400 additional units, which will be known as the Trove. We continue to plan the ground-up development of approximately 550 units on site at Riverside Apartments expected to commence in the second half of 2018.

And finally on retail, we grew occupancy by 420 basis points on a year-over-year basis in 2016, primarily due to several large leases that commenced during that year. We continued to experience strong rental growth from smaller in-line retailers and have noticed a pickup in consumer confidence over the past quarter. At approximately 96% occupied, we are driving additional revenue through specialty leasing and short-term opportunities. Another retail NOI growth driver is the development of a two-story mixed use building on site at Spring Valley Village. We will be utilizing additional on-site density to expand this high quality shopping center located in one of Washington, D.C.’s most affluent neighborhoods. We expect to spend approximately $5 million and generate incremental stabilized annualized NOI of approximately $500,000 over 2016 NOI.

To conclude, we expect 2017 to be a strong year for our region. Growth continues to be driven by an expanding private sector, which has created approximately 24,000 professional and business services jobs over the past 12 months, relative to an average of 10,680 jobs between 2000 and 2015. In 2016, the year-over-year rate of job growth in the Washington Metro region exceeded that of New York, Los Angeles, Chicago and Boston. Moreover, following the national elections, we are seeing greater levels of activity in the region as associations, corporations, lobbyists as well as accounting and law firms ramp up to influence and position for the proposed initiatives of the new administration.

At this time, we are more optimistic about the prospect of increased private sector growth than concerned about federal hiring freezes for three reasons. First, federal government leases accounted for less than 1% of our 2016 revenue and our portfolio doesn’t directly compete with GSA’s strongholds such as NoMa, Southwest, Crystal City, Springfield or Bailey’s Crossroad. Second, our regions dependence on the federal government has already shrunk dramatically, from approximately 40% of our gross regional product in 2010 to between 30% and 35% today and is heading to 27% by 2021. Today, the government leases just over 10% of space in the core markets where we compete.

Finally, our region has already experienced recent years of executive orders focused on reducing the size of the federal footprint. And the GSA is now several years into its rightsizing process. As per JLL Research, GSA space reductions averaged 15% to 25% per year from 2011 to 2014, while recently completed prospective level deals averaged just over 10% in space reductions. This implies that while the government’s rightsizing process may not yet be complete, it should provide diminishing rates of return in space compression in the years ahead. The consensus view is for alignment across the House, Senate and White House to alleviate political gridlock, which in turn should lead to the Congress enacting more legislation. If historical correlations hold, increased legislation should spur greater net absorption within the private sector and we should begin to see this region’s real estate fundamentals return to higher levels of growth.

Now, I would like to turn the call over to Steve to discuss our financial and operating performance in 2016.

Steve Riffee

Thanks, Paul. Good morning, everyone. 2016 net income of $119.3 million or $1.65 per diluted share exceeded 2015 net income of $89.7 million or $1.31 per diluted share largely due to higher gains on asset sales, lower interest expense and higher income from real estate. We reported core FFO of $1.76 per diluted share for full year 2016, the midpoint of our most recent guidance range. This represents approximately 3% core FFO growth over 2015 core FFO per diluted share of $1.71, while partially absorbing dilution from asset recycling in equity issuance.

Core funds available for distribution or core FAD was approximately $102 million in 2016, representing an 85% payout ratio, which was in line with our projections. We continue to target an annual core FAD payout ratio in the mid-80s. 2016 same-store NOI grew 1.2% over the prior year. Same-store rents increased 160 basis points over full year 2015 and same-store physical occupancy improved 220 basis points over the prior year to end 2016 at 94.3% occupied.

Starting with office, 2016 same-store NOI grew 1.4% over the prior year, exceeding our most recent guidance of approximately 1%. Same-store office rents grew 180 basis points over full year 2015 primarily due to annual rent increases across our D.C. office portfolio. Same-store office physical occupancy improved 110 basis points over the prior year to end 2016 at 92.1%. We leased approximately 600,000 square feet of office space in 2016 driven by approximately 440,000 square feet of office renewals, which brought our 2016 office tenant retention rate to approximately 70%.

In the fourth quarter, we renewed approximately 65,000 square feet of space and achieved an 8.1% improvement in GAAP and a 1.3% improvement in cash rent spreads. Our approximately 39,000 square feet of new leases were 5.7% higher on a GAAP basis, but negative on a cash basis in the quarter, impacted by one short-term lease where we accepted a face rent reduction in exchange from minimal buildout and zero free rent. Our same-store Washington DC office portfolio continues to outperform the region with the year end occupancy approximately 390 basis points above overall DC market occupancy. Our office portfolio is also significantly outperforming in Northern Virginia, where our year end occupancy is approximately 11% higher than market. Our overall office portfolio was 91.1% occupied as of year end 2016.

Moving on to retail, in 2016, our portfolio experienced strong same-store rental growth of 230 basis points over full year 2015. At year end 2016, same-store physical occupancy was 95.7% or 420 basis points higher than at year end 2015. Retail same-store NOI was approximately flat for full year 2016 in line with our most recent guidance while also absorbing the fourth quarter bankruptcy of Offenbachers, a regional retailer occupying approximately 18,000 square feet. We leased approximately 2,000 square feet of retail space in 2016 driven by approximately 170,000 square feet of renewables, which brought our 2016 retail tenant retention rate to approximately 80%. In the fourth quarter, we renewed approximately 66,000 square feet of space and achieved a 10% GAAP and a 7.8% cash rent increase on renewals. For 2016, retail new leases were 15.4% higher on a GAAP basis and 3.5% higher on a cash basis.

Moving on to multifamily, our 2016 full year same-store NOI was 2.7% higher year-over-year partly due to same-store physical occupancy improving 190 basis points and same-store rents increasing by 30 basis points in 2016 over 2015. Excluding the fourth quarter bankruptcy of a restaurant located within one of our multifamily properties, 2016 same-store multifamily NOI would have grown by 3.3% over 2015. On a per unit basis, the same-store portfolio ended the fourth quarter 96.3% occupied.

Now turning to 2017, our core FFO guidance is expected to range from $1.74 to $1.82. The year-over-year growth embedded in our current portfolio is skewed by the timing of the 2016 recycling execution. It’s a dilution from our 2016 asset recycling that all occurred on January 1, 2016, then 2017’s guidance would represent approximately 7% core FFO growth on a pro forma basis at the midpoint. We are currently not providing guidance relating to acquisitions or dispositions for 2017, but remain a local sharpshooter, looking for value-add opportunities and we will update you on future calls to the extent that we can execute on such opportunities.

Our guidance includes the following assumptions. Our same-store NOI growth of 4.75% to 5.25%, office same-store NOI growth of 7% to 7.5%, retail same-store NOI growth of 3% to 3.5%, and finally, multifamily same-store NOI growth of 2.5% to 3%. We have removed Braddock Metro Center from the same-store portfolio, as we plan to reposition the asset prior to the re-tenanting that Paul commented on earlier. We project office non-same-store NOI to range between $9 million and $10 million and multifamily non-same-store NOI to range from $13 million to $13.75 million. Our interest expense is expected to range between $46 million to $47 million. G&A is expected to be between $19 million to $20 million.