Federal Reserve Maintains Low-Rate Policy

The Fed hit “pause” in May, keeping its benchmark rate unchanged.

The group cited labor market and inflation conditions that are still within expectations. Not too hot, but not too cold, either.

Interestingly, the post-meeting announcement addressed slowing economic activity, even as the economy in whole continues to strengthen.

The Fed could be leaving its options open for its June meeting. A hike is fully expected next month, but the Fed may be hinting that it’s not a sure thing.

That could be good for mortgage rates today.

Click to see today’s rates (May 3rd, 2017)

Fed: We’re Keeping Rates Low

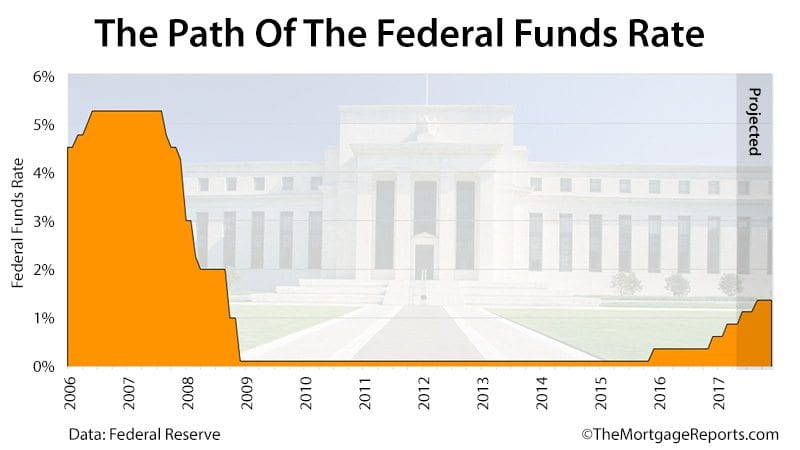

Wednesday, the Federal Open Market Committee (FOMC) voted to maintain the Fed Funds Rate at a range between 0.75-1.00 percent.

That’s low by historical standards.

As recently as 2007, the federal funds rate topped 5%, meaning rates for credit cards, home equity lines of credit, and other consumer credit accounts were at least 400 basis points (4.00%) higher than they are today.

Mortgage rates were past 6%.

Seeking to maintain current growth, the Fed is keeping borrowing costs low across the board with its “no-hike” decision.

But the Fed is data-dependent, it reminded markets. The group’s future moves will depend on the strength of labor markets, and on the pace of inflation within the economy.

The Fed’s mandate is to balance those two forces.

Currently, labor markets are improving with job gains “solid” in recent months. The economy has now added more than 15 million jobs since 2010.

Job growth may ignite inflationary forces. Wages are ticking up. The Fed may need to increase rates to cool rising price increases within the economy.

The Fed aims at two percent inflation per year. Currently, inflation is running closer to 1.6%.

That could rise quickly, with the current on-fire stock market, rising oil prices, and unemployment at its lowest level since 2007.

The Fed used its statement to identify inflationary threats within the economy and to suggest the direction of future policy (emphasis added):

The Committee expects that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

In plain English, this says that the Fed will raise the Fed Funds Rate at a speed appropriate to the pace of inflation. Inflation rates are running low, but not alarmingly so. Future hikes will be gradual to lift inflation to the Fed’s target.

Note that monetary policy can take a long while to work its way through the economy — sometimes three quarters or more. A June rate hike, for instance, would not be felt through the economy until 2018.

The Fed is planning ahead.

Click to see today’s rates (May 3rd, 2017)

Fed Outlook For The Rest Of 2017

The May Fed meeting presented no surprises to markets.

While the post-meeting announcement mentioned weaker economic activity of late, it also argued that the economy is doing well.

Consumer spending is strong, and unemployment is at 10-year bests.

Of significance to the mortgage shopper is the Fed’s continued policy of reinvesting principal payments on its massive holdings of mortgage-backed securities, or MBS.

As mortgages are paid down, cash is freed up on the Fed’s balance sheet. The Fed then uses that cash to buy more MBS.

That helps mortgage rates by keeping supply down and demand up. The higher demand for MBS, the lower mortgage rates will be.

If the Fed were to stop reinvesting, or worse — start selling — mortgage rates could rise significantly. For now, the Fed vows to maintain its stance on reinvestment until the federal funds rate approaches historically normal levels.

As a mortgage shopper, it’s a very good time to lock a rate.

Lenders are now offering 30-year fixed rate VA and FHA mortgages in the low-4s. Conventional loan rates aren’t much higher.

According to Ellie Mae, a software provider that processes millions of applications per year, lenders are issuing loans at the following average rates:

- Conventional loans: 4.50%

- FHA loans: 4.32%

- VA loans: 4.10%

Today’s rates are holding well below the historical average of more than 8%.

What Are Today’s Mortgage Rates?

Mortgage rates remain cheap and the Federal Reserve appears intent on keeping them in check. Markets often change without notice, however. Lock a loan while rates are still low.

Get today’s live mortgage rates now. Your social security number is not required to get started, and all quotes come with access to your live mortgage credit scores.

Click to see today’s rates (May 3rd, 2017)

The information contained on The Mortgage Reports website is for informational purposes only and is not an advertisement for products offered by Full Beaker. The views and opinions expressed herein are those of the author and do not reflect the policy or position of Full Beaker, its officers, parent, or affiliates.

Try the Mortgage Calculator

Try the Mortgage Calculatorfederal-reserve-maintains-low-rates-no-hike-until-at-least-june

No comments:

Post a Comment