Quicken Loans is built for the “click here” generation, people who think doing business face-to-face is overrated. In fact, it famously describes the application process on its Rocket Mortgage interface as, “Push button. Get mortgage.”

Quicken/Rocket provides just about all the services your neighborhood lender does: Fixed- or adjustable-rate home loans, mortgage refinancing, FHA and VA loans and “jumbo” loans. It’s not only the biggest online mortgage lender in the U.S., it’s the third-largest home loan lender — online or otherwise — behind Wells Fargo and Chase, according to trade publication Mortgage Daily. It originated a whopping $79 billion in mortgages in 2015.

Here’s how Quicken Loans and Rocket Mortgage stack up.

AT A GLANCE

- Minimum credit score: 620 (580 for FHA loans).

- Fixed loan terms of 8-30 years.

- ARMS with fixed-rate terms of 5, 7 or 10 years.

- No origination fee.

An online mortgage lender goes even more virtual

Quicken Loans was already an online lender, but it repositioned itself as even more virtual when it introduced Rocket Mortgage — which is a service portal, not a separate company. Beneath the new Rocket technology are the same underwriting standards of the Quicken mother ship.

You can speak with a mortgage advisor anytime by pushing the “Talk to Us” button on every Rocket Mortgage page, but the site caters to self-service users who want to apply for a home loan without talking to a human unless it’s absolutely necessary.

“What Rocket Mortgage does is, it gives the client the ability to price their own loan, pick their interest rate, the points, understand the trade-off to go with a higher rate and less points, et cetera,” says Bob Walters, chief economist of Quicken Loans. “It allows them to lock that interest rate. It allows them to e-sign and create the original application without speaking to anyone.”

What Rocket Mortgage does best

- Instantly verifies employment and income for more than 60% of working Americans.

- With your authorization, downloads asset statements from 95% of U.S. financial institutions.

- Tells you the loan amount you’ll qualify for within minutes.

- Offers custom fixed-rate loan terms of between 8 and 30 years.

- Provides first-time homebuyers FHA-backed loans, as well as products offered by Freddie Mac and Fannie Mae that require down payments as low as 3%. “Quicken Loans is the largest and highest-quality (lowest default rate) FHA lender in the country,” according to a company-provided data sheet.

Rocket Mortgage’s document and asset retrieval capabilities alone can save you a bunch of time and hassle. Eventually every lender will do this — or be left behind.

Considering fees and mortgage rates

“One of my great pet peeves in this industry over the years has been a lot of people advertise a low rate with a bunch of asterisks, and then by the time you get into the process, you realize that’s not the rate you’re going to get,” Walters says.

But he also thinks the days of low advertised rates with fine-print disclaimers are fading fast. He says the industry is now so highly regulated — and becoming so transparent — that every lender’s fees and mortgage rates are nearly the same.

One fee distinction: Quicken/Rocket doesn’t charge an origination fee. Many traditional lenders — such as banks, credit unions and mortgage brokers — do.

Rocket Mortgage users

Rocket Mortgage users are more likely to buy than refinance. They’re also slightly younger and tend to have a little bit better credit than Quicken Loan users, according to Walters.

“Client focus and technology: That’s what differentiates us,” Walters says. Another distinction, he says: Quicken Loans doesn’t sell its loans to servicers. In other words, you don’t get the mortgage from them, only to deal with a different company down the road.

“I think that branch loan officer is a dying profession.”

Quicken Loans has been awarded six consecutive J.D. Power customer satisfaction awards for loan origination. Walters believes that’s a sign of things to come.

“I think that branch loan officer is a dying profession,” he says.

How Rocket Mortgage works

To put Rocket Mortgage to the test, we went through a step-by-step demo with Regis Hadiaris, the tool’s product lead.

To put Rocket Mortgage to the test, we went through a step-by-step demo with Regis Hadiaris, the tool’s product lead.

If you apply for a purchase mortgage or refinance through Rocket, you’ll first create an account and provide the usual personal information. For instance, to apply for a refinance, you’ll input your current mortgage details. Typing in your home’s address automatically imports property data, including the year your home was built.

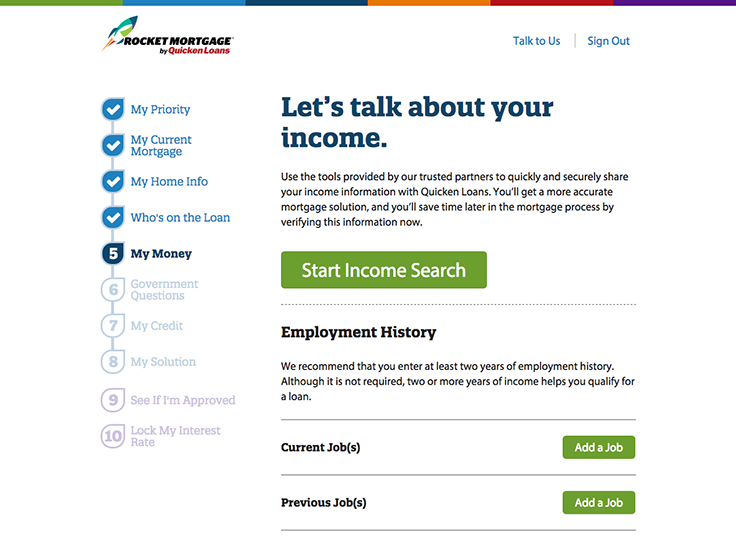

You can add income details yourself, or, if you provide your birthday and Social Security number, the system will perform a search and fill them in for you.

“What’s nice about this is two things,” Hadiaris says. “It makes it easier for the person filling out this information, but at the same time, the system has done an electronic verification of income already, so it is actually starting the process of doing income calculations.”

Those calculations are a proprietary analysis of your income information. Algorithms are beginning to build your customized home loan recommendations.

Next, you’ll enter your asset information, or have it automatically imported. Rocket can pull data about products such as checking, savings and investment accounts from 95% of U.S. financial institutions.

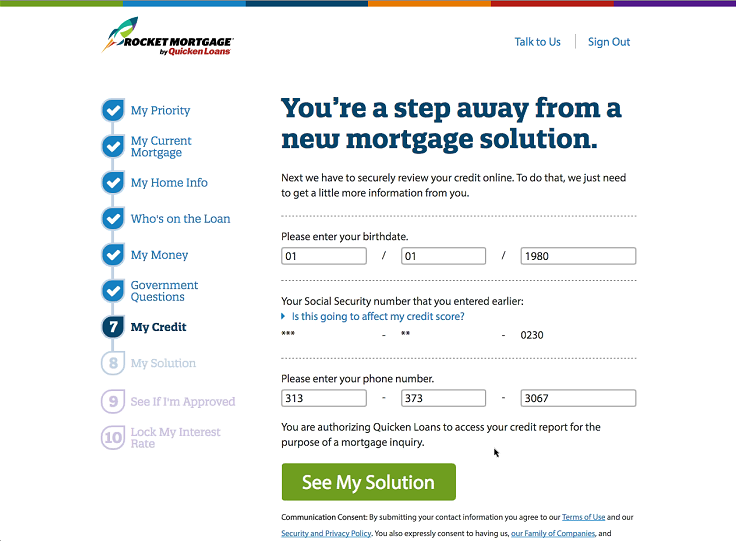

Once the system has your data, you’ll come to a big green button that says “See My Solution.” This is where “Push button. Get mortgage” comes into play.

Once the system has your data, you’ll come to a big green button that says “See My Solution.” This is where “Push button. Get mortgage” comes into play.

When you click the button, Rocket gathers your credit score and history from all three credit bureaus, and compares the results with Quicken Loans’ mortgage underwriting guidelines.

An entertaining “T-Minus” countdown appears on the screen. After a few minutes, it’s replaced by details about your customized mortgage options. Slider bars allow you to change the closing costs, loan term and interest rate until you’re happy with the results. Then click the “See If I’m Approved” button, and within minutes you’ll get a loan approval — or not.

If you’re approved, you can lock your interest rate and print out an approval letter, then hit the road and start house hunting. Once you have a purchase contract on a home, the loan details are finalized, and the package goes through the usual underwriting process: ordering an appraisal, verifying a clear title and all the rest.

If your loan application is denied, you can speak or chat online with a mortgage banker to find out why and what you can do to be approval-worthy.

Where Quicken Loans and Rocket Mortgage fall short

Even though Quicken/Rocket is a leading full-service lender, there might be drawbacks for some customers:

- Quicken/Rocket doesn’t offer home equity loans or home equity lines of credit.

- If you’re a “look me in the eye” type of customer, you’re out of luck.

- Quicken Loans doesn’t consider alternative credit data. It just looks at credit scores and debt-to-income ratios, the way most mortgage lenders always have.

If you like to shop online and enjoy using a streamlined and efficient app, with live help a quick click away, Quicken Loans and Rocket Mortgage might be just what you’re looking for.

More from NerdWallet:

How Much House Can I Really Afford?

Compare Mortgage Rates

Find a Mortgage Broker

Hal Bundrick is a staff writer at NerdWallet, a personal finance website. Email: hal@nerdwallet.com. Twitter: @halmbundrick.

Need to get preapproved?

Find a lender and get preapproved to show you are a credible buyer.

You might also like:

Quicken Loans and Rocket Mortgage Review 2016 - NerdWallet (blog)

34 comments:

Nice one dear!

Quicken Technical Support +1-877-773-3202Toll Free 24*7. If you're looking for the Quicken Support contact number. Then this is the best phone number +1-877-773-3202 to the Quicken customer service.

Quicken Customer care

Quicken Customer helpline number

Awesome post! If you're looking for the Quicken Support contact phone number. In that case this is the top phone number +1-855-560-0666 to the Quicken customer service.

avg Customer helpline

avg support number

avg helpline number

Great post ! But we are on a mission to maximize customer satisfaction by providing right information on all the queries asked for HP Laptops & Computers. With full involvement in the customer support services our team manages more than hundreds of phone calls in a day. There’s no delay from our side in answering your calls and our amazing tech support engineers are well aware of new computer technologies.

Hp Printer Help Numbers

Hp Support phone number

hp helpline humner

hp support number

Thank you for sharing such great information.

It is informative, can you help me in finding out more detail on

quicken loans.

Bluehost web service

Bluehost customer service

Godaddy customer service

Godaddy Web hosting service

Binance support phone service

Bitcoin help support service

nice blog with useful information..thanks for sharing with us...

quicken technical support number

I have read so many blogs on this topic but this post is actually a fastidious. I read many blogs to know about Rocket Mortgage but here i found such a great information. Thanks in favor of sharing such a fastidious idea, piece of writing is nice.

A wonderful blog on Mortgage Loans In Hyderabad. Taking mortgage loans against a house or a commercial land is always a good option especially for the retired individuals who are in need of lumpsum amount. People buy houses which are very new and sometimes an old house that can be renovated later, for such old houses also you can expect the loan from banks as well as other NBFC's. Great article, thank you.

I recently got a loan from Cashry. They helped me find a lender so that I could borrow some money. The borrowed money was used for my mother’s treatment and it was a great help in that situation for me.

waooo !!! that's great, I need to Buy real active Instagram Follower . Thank you. :)

Really This goes far beyond the commenting! It wrote his thoughts while reading the article amazingly : buy instagram followers cheap

The material which is used to read for us very appreciable. I also exploring for about Buy Instagram Followers Canada . Your information is so amazing keep it up. Thanks

Thanks for sharing such a nice and informative post. I Really appreciate Your work. I am actually enjoy establishing your post.

Buy Instagram Likes UK

Keep Sharing Quality Content. Active Followers Provides Active and Real Followers to Grow your Bussiness online so Buy Instagram Followers UK today.

Get social media services at cheap rates Buy active Instagram Followers uk and likes at the lowest price what you need if you will get all things at one place, secure payment via PayPal, money-back guarantee 24/7 customer support.

I am gonna love your blogs and your personal profile as well. The information you are providing is worthy.

Keep on doing such activities that are helping others in this digital world. I am also helping others on social media through IG likes.

Buy Instagram likes UK at cheap rates to get loved by more.

It is very interesting article that you written here. Really I’m not related to this, but I think it is the greatest opportunity to learn and read more about, And as well talk about a different topic to which I used to talk with other social services as Buy Real Instagram likes.

it was a great effort you are doing for us . Such an impressive keep doing this

buy Instagram followers and make your own world in the society of social media

buy Instagram followers

Nice work. Keep it up. Also view

Buy instagram followers UK

I am gonna love your blogs and your personal profile as well. The information you are providing is worthy. Keep on doing such activities that are helping others in this digital world. I am also helping others on social media through IG likes. Buy TikTok likes UK at cheap rates to get loved by more.

https://www.quora.com/What-are-the-roles-of-packers-and-movers-in-moving-a-home

https://www.skydrive.pk/2017/12/what-is-falling-action-of-will-come.html?showComment=1600930444112#c6464176095636419740

http://techspotusa.com/pages/forum-thread-view?r=T9HO7BCQF7&send_to=%2Fpages%2Fforum%3F407_advanced%3Dfalse%26407_page_number%3D36#software_comment_1148

https://troprouge.com/2016/08/09/postcards-from-london/#comment-22681

https://www.primarypunch.com/2016/06/tickled-pink-tags.html?showComment=1601114359812#c9179381844717587080

https://krestaintheafternoon.blogspot.com/2011/03/misconduct-by-government-employees-is.html?showComment=1601114611020#c2356791695213155588

http://www.namelessfashionblog.com/2020/05/moving-with-style.html?showComment=1601116654273#c161739946349497619

The article that is shared by you at that site is very informative and also motivational, please check: Buy Instagram Followers UK Thanks.

If you are careful and do everything correctly then there is no reason why you cannot find out the perfect mortgage for your needs and that will mean that you can enjoy buying your first home.

anchor text

Impressive content really appreciate your efforts, if anyone needs organic Instagram followers can visit our site. buy instagram followers uk

legit likes is a top-rated website where you can get social media services at an affordable price. visit now and buy Instagram followers uk to increase your social presence.

If you are planning to buy Instagram followers in good numbers then buy Instagram followers from a good service provider and get assured and safe results within a very short period of time. Choosing the website plays the trick to success.

buy real Instagram followers as more followers are the indication that whatever you advertise or deal on Instagram is legitimate, the same trust can bring forward more followers and this is how you build a cohesive community on Instagram.

appreciate your work

BUY INSTAGRAM REAL FOLLOWERS ,VIEWS AND LIKES UK

buying Instagram followers is very important now it help in boosting your business getting followers organically take a long time but buy real Instagram followers

help you to make it essay

You can battle spam by adhering to a predictable posting plan. To abstain from spamming, brands should just post a couple of times each day. Be that as it may, it doesn't make any difference what your posting recurrence is, you need to keep it steady. There are around 200 million Instagram clients who sign on consistently.

Tshirt printing

There are a number of benefits to buy Instagram followers. For starters, you can increase your following quickly and easily. You can also use your followers to promote your business or blog posts.

Great blogging,Thanks you to sharing a very informative and sensitive site.When i read this blog i feel happy and i like it.nangs near me

Fantastic page! I actually really liked all the following. I hope to learn from you. I've got outstanding awareness and so perception.

I’m certainly absolutely fascinated by this particular guidance.

Buy Instagram Views Uk

Post a Comment